Boost Debt Recovery with Smart Collection Automation

Here is a scene I hear far too often when I speak with CX and collections leaders.

It’s the 10th of the month.

Your collections team is working the phones at full throttle. Some agents are chasing down small-ticket overdue payments; others are trying to convince high-value customers to restructure their loans.

Meanwhile, dozens of calls go unanswered, customers dodge numbers they don’t recognize, and your agents are left juggling outdated systems, manual follow-ups, and the stress of “collect more with the same team.”

Does this sound familiar?

Throwing more agents at the problem doesn’t scale anymore.

Here’s the reality:

- Customers are harder to reach.

- Regulations are tightening.

- Debt volumes are increasing.

- And budgets for collections aren’t growing in proportion.

That’s why the smartest collections organizations are asking:

How can I increase recovery rates without simply adding more people?

The answer lies in smart collection automation where AI-powered debt recovery is reshaping the debt collection industry and helping scale outcomes without simply adding more people.

4 Challenges in Debt Recovery Leaders Face Today

Changing Customer Behavior

- Do your customers prefer self-service over phone calls?

- Do your customers screen calls via apps like Truecaller?

- Does your number get marked as spam by the telcos?

- Do your customers expect to pay via digital wallets, UPI, or even in-app payment links, not just checks or bank transfers?

Regulatory Pressure

- FDCPA, DRA, Reg-F, DoT, and TRAI rules in India are stricter than ever. You cannot send collection agents home unless they are certified by DRA. You cannot call them before or after a specific time of day. Besides, you cannot try to reach someone beyond a certain number of times.

- Regulators have become very strict against aggressive or intrusive collection practices.

- In today’s environment, even a small slip in debt collection compliance can destroy reputations overnight

High Agent Attrition

- Collections is a stressful job, and the burnout is real.

- High turnover results in constant hiring and retraining, adding cost without improving recovery rates.

Rising Debt Volumes

- Inflation and economic downturns have increased delinquency rates.

- More accounts to chase, with the same or fewer people doing the chasing.

Traditional Debt Collection Bottlenecks Slowing Recovery

If you’ve worked in collections long enough, you know the usual suspects:

- Agents spend too much time dialing numbers, leaving voicemails, logging call outcomes, and chasing follow-ups.

- You follow a cookie-cutter approach. Every delinquent account receives the same script and call pattern, regardless of its history or likelihood to pay. That’s a lot of wasted effort.

- Is your customer data spread across CRMs, loan management systems, and call logs? A modern call center debt collection solution can unify these silos, giving agents a single view of the customer instead of leaving them to operate in the dark.

- Do accounts that should move quickly to legal or restructuring often get stuck in endless cycles because of your ineffective outreach?

- Manual dialing increases the risk of calling outside allowed hours, missing disclosures, or failing to log interactions accurately.

This is a lot of effort with less-than-expected results.

What Is Smart Collection Automation?

Smart collection automation employs AI, analytics, and workflow orchestration to:

- Divide accounts into groups and decide which ones to contact first, based on how likely they are to recover.

- Based on the customer’s age, gender, and delinquency status, it helps you choose the best way to reach them, such as SMS, WhatsApp, email, IVR, or a live agent.

- Identify the optimal moment to contact clients when they are most likely to respond.

- Set up automatic reminders, payment link sharing, and follow-ups for repetitive tasks.

- Ensure that the collection process has built-in compliance guardrails.

AI handles the bulk of the work through smart collection automation, allowing agents to focus on the most complex instances where human judgment is crucial.

Here are a couple of use case examples

One of our fintech customers automated SMS/WhatsApp payment reminders with dynamic payment links, leading to 30% faster repayments in the 1–30 day bucket.

A collection BPO customer reduced agent attrition by 15% after automating repetitive dialing tasks, because agents spent more time on meaningful conversations.

Key Benefits of Debt Collection Automation

When I talk to collections leaders in India, the question is always the same:

How do we improve recovery without adding another 200 agents to the payroll?

The truth is, smart automation works best where delinquency volumes are high, customer channels are fragmented, and compliance is tightening.

Here’s how it plays out.

Higher Recovery Rates

The biggest challenge is in getting customers to even pick up the phone. Many people use Truecaller to block unknown numbers, while younger borrowers often simply don’t answer calls.

Automation solves this by matching the right channel to the right customer.

For some, it’s WhatsApp with an instant payment link.

For others, it’s an SMS reminder in their regional language.

High-risk buckets still get live calls, but only after the system predicts the best time to reach them.

Let me give you an example.

One of our NBFC clients divided its consumers based on how much they used digital technology. The AI-driven system sent tech-savvy borrowers on WhatsApp and IVR calls in their native language to rural borrowers. This led to 22% more right-party contacts in the first 30 days of delinquency.

Lower Cost Per Collection

Collections often require a lot of agents making repetitive calls. However, hiring more people is costly and not feasible when Net Interest Margins are low.

Smart automation reduces the cost of collections by automating simple operations, such as sending reminders, tracking responses, and generating payment links. This means that agents only have to deal with more complicated instances.

Let me give you an example.

One of our digital lending customers automated payment reminders via SMS, WhatsApp, UPI, and IVR for the 1–30-day bucket. Borrowers received SMS and WhatsApp nudges with UPI payment links. 30% of dues were settled digitally, without a single agent intervention, cutting the cost per collection significantly.

Agent Productivity and Morale

Sitting in a call center, dialing hundreds of numbers, only to be hung up on, is mentally draining, to be honest.

This burnout is one of the key reasons for high agent attrition in collections, making automation a critical lever for productivity and retention.

Automation makes things easier. Agents don’t waste time going after leads that aren’t going anywhere. Instead, they deal with high stakes, high-value talks, including negotiating with MSME owners who want to pay but need a restructured schedule.

This makes their jobs more interesting and keeps them from getting burned out.

Let me give you an example.

One of our BPO customers used AI to filter out “low-propensity to pay” accounts. Agents focused only on promising customers. Attrition dropped by 15% in six months, and recoveries improved because conversations were more productive.

Better Customer Experience

Customers often complain:

The bank kept calling me ten times a day for a small overdue bill.

This not only damages customer trust but also invites regulatory scrutiny.

Smart automation elevates customer experience in debt recovery by creating a gentler, more respectful process with nudges across WhatsApp, SMS, and IVR—without constant interruptions.

They can click a UPI link, pay instantly, and move on.

Let me give you an example.

One of our telco customers automated overdue bill reminders via WhatsApp. Customers got a friendly message with a “Pay Now” button linked to UPI. Complaints about harassment calls dropped by 40%, and on-time payments went up.

Built-In Compliance

Regulators are becoming stricter about fair collection practices. The RBI has already warned people about aggressive recovery agents and too many calls.

Smart automation ensures compliance is part of the system and process:

- Don’t ever make calls outside the permitted hours.

- Automatically include required disclosures in scripts.

- Log every interaction.

Let me give you an example.

A microfinance customer of ours reduced compliance violations by 70% after moving to our system that enforced RBI’s call-time regulations automatically.

Scalability

Collection volumes are rising with digital lending growth. But adding more people is not the answer.

Automation scales effortlessly.

Whether your delinquency bucket grows by 20% or 200%, the system handles the load, while agents focus only on cases where human intervention is truly required.

Let me give you an example.

During COVID-19, one of our NBFC customers experienced a threefold increase in defaults. They didn’t hire hundreds of new agents; instead, they used technology to handle early-stage accounts digitally. Human agents solely dealt with escalations, which kept recovery costs down.

Automation isn’t just about efficiency. It is about protecting your business from the triple squeeze of rising delinquencies, shrinking margins, and regulatory risks.

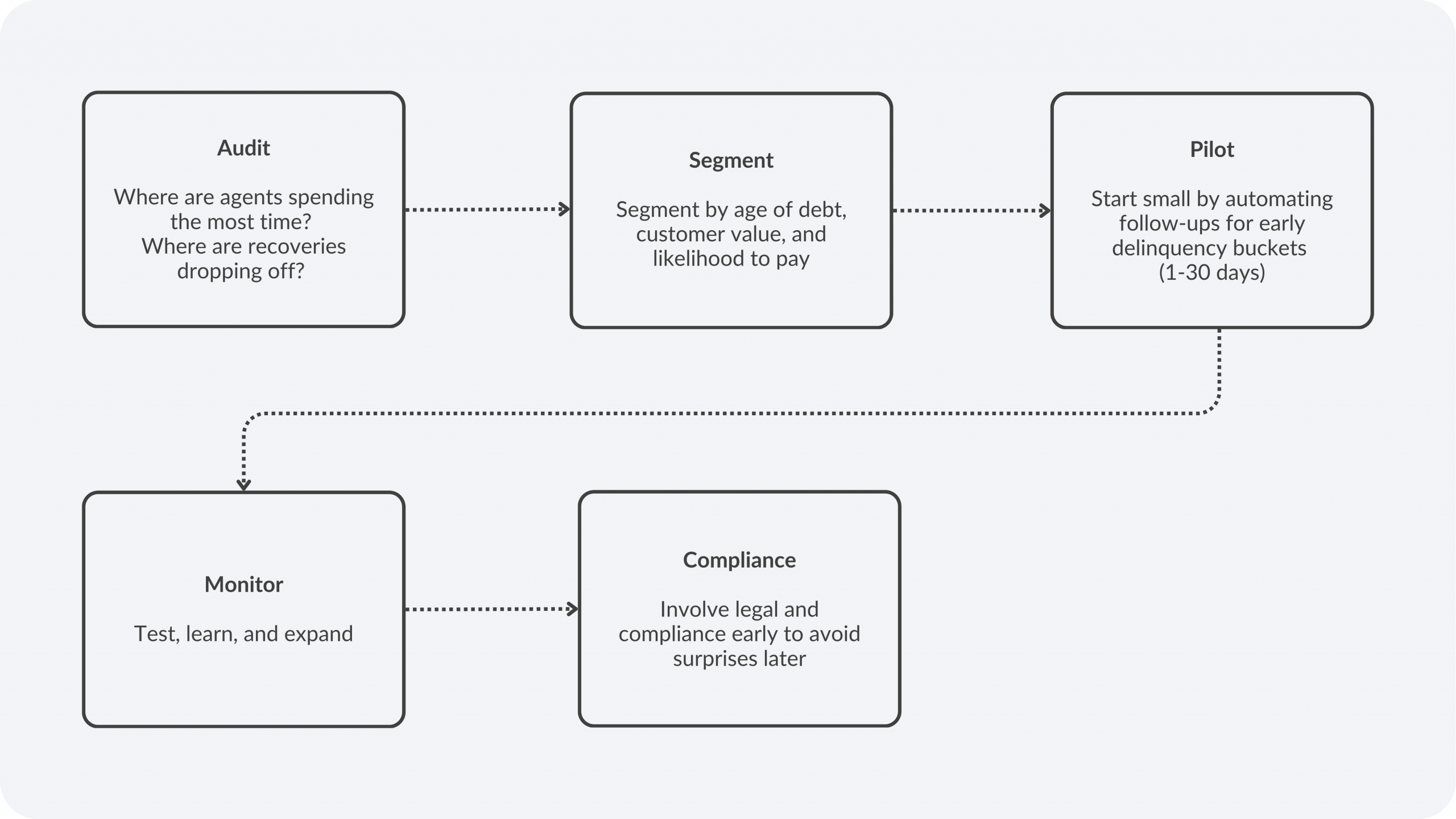

How Leaders Can Get Started with Debt Collection Automation

Phases of Smart Automation Adoption

1. Phase 1: Assistive Automation

Automate simple reminders (SMS, emails) and dialer workflows. Agents still lead the process.

2. Phase 2: Intelligent Orchestration

AI decides which accounts get which outreach, at what time, via which channel.

3. Phase 3: Proactive Self-Service

Customers can resolve delinquencies directly via payment links, chatbots, or IVR without ever speaking to an agent.

4. Phase 4: Predictive and Preventive

AI predicts who is likely to default and intervenes early before debt even becomes delinquent.

Debt Recovery Automation Checklist for Leaders

Here’s a simple checklist before you dive in:

- Have we mapped our current workflows end-to-end?

- Do we know which delinquency segments are best suited for automation?

- Are compliance/legal stakeholders aligned?

- Do we have data integration across CRM, LMS, and dialer?

- Have we defined success metrics (e.g., right-party contact rate, cost per collection)?

- Do we have a clear escalation path from automation to an agent?

Choosing the Right Collection Automation Partner

When you’re shopping for solutions, ask vendors tough questions:

- How good is their channel optimization and segmentation?

- Can it integrate with your existing CRM/LMS?

- Are local and global compliance standards built in?

- Does it give you real-time insights?

- Can it handle your growth over the next 5 years?

- Will they handhold your agents through the transition?

Remember, you’re not buying software; you’re buying confidence in recovery outcomes.

Debt recovery doesn’t have to mean bigger teams, longer hours, and higher burnout.

The real leaders I see succeeding today are the ones who shift the question from:

How do we add more agents?

to

How do we add more intelligence?

If you’re leading a collections function today, you don’t need to chase every shiny AI promise.

Start small, focus on the right buckets, measure outcomes, and scale step by step.

Success in collections isn’t about chasing debtors harder. It’s about making recovery smarter.